OilPrice.com

OilPrice.com - While it appears that Russia has been refusing to send extra natural gas to Europe during the current shortage, the continents energy crisis may have been caused by something else

- Putin has long understood the significance of the liberalization of European gas markets, and algorithmic trading may have played a part in soaring prices

- If Russia was indeed able to manipulate prices higher by using ‘paper volumes’, then the security of Europe’s broader energy market will have to be looked at

The continuing European energy market crunch is still making headlines. The main culprit, according to media and politicians, is Russia, as it is refusing to increase its gas deliveries to the market. When looking at market fundamentals, it certainly appears that Russia is partly responsible for the energy shortage, but there is a major underlying issue that is not being covered. Putin has weaponized the energy markets by using an intricate web of trading instruments, media attention, and supply-side control. Russia has been playing pipeline politics with oil via the OPEC+ agreement and with natural gas via its control of European markets. After warning European leaders several times in recent years, Putin now seems to have used the financialization of energy markets, aka paper values and not volumes, to his advantage.

In recent years, Putin has been looking to use the changing European gas market to his advantage. Europe’s liberalization of its domestic gas markets combined with a full focus on spot market options, such as TTF and others, removed long-term contracts as a primary source. Long-term contracts, based on oil-price indexed contracts, were seen as the main constraint to liberalization and lower price settings. This change to spot contracts was due to Europe’s desire to become less import-dependent on Russian natural gas while opening up to international LNG options. For the first years, this change worked well, as prices went down and diversification, at least on paper, increased.

More recently, however, the situation changed dramatically and Russia once again gained the upper hand. While European politicians were focusing on Ukrainian gas pipelines or Nordstream 2, the internal function of the European gas market was largely ignored. In reality, the liberalization of gas markets, especially in Europe, put more power into the hands of independent gas trading groups, including Gazprom.

Without pushing for a direct confrontation, Russia was able to play with market fundamentals. The push by European nations to go all-out on renewables, discarding the idea of gas as the transition fuel of choice, threatened Russia’s future. Putin and his supporters warned Europe that there could be major repercussions for that move, but the message fell on deaf ears in Brussels.

It seems that Europe’s politicians failed to understand a major threat in modern international gas trading, namely the role of new technology and algorithms. Putin’s advisors clearly understood both the positive and negative options associated with putting gas market futures and deals in the hands of algorithm-based systems.

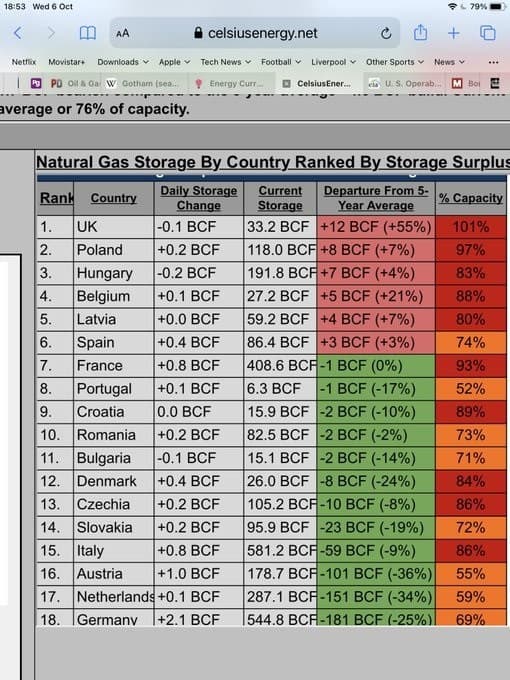

An in-depth analysis of current gas markets, including EU and UK gas storage volumes, is partly clouding the overall real situation. There is doubt that current gas storage volumes are lower than before, however, no real attention has been given to the fact that one of the main drivers behind the current energy crunch and extremely high prices, which are to the advantage of Putin, are caused by 3rd party moves.

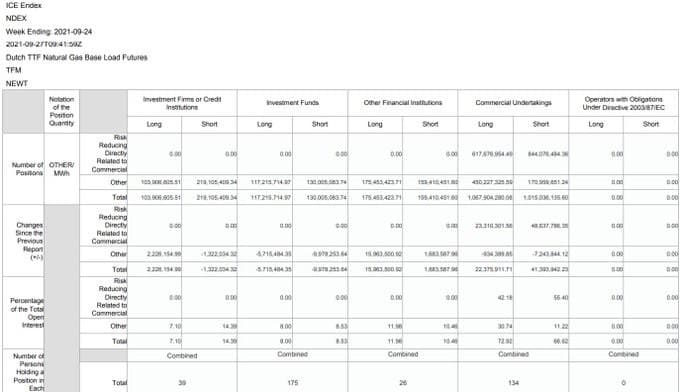

In recent months, financial players and traders have been committing to extreme high hedging and speculative positions, not only in natural gas markets but also in electricity markets. Analysis of the commitments of traders report ICE Europe data on TTF futures trading shows that speculation has been a major driver behind the current price spikes and shortages. Putin has been able to use the system of natural gas and electricity markets to his own advantage, aka weaponizing his own energy trade position in the market.

Related: A Very Predictable Global Energy Crisis

As a trader stated, while Europe wanted its own energy exchange (EEX) to hold market power, the reality is that the EEX is not even close to ICE Endex and ICE Europe. Taking into account US CME/NYMEX and ICE US Energy Division, EEX is being dwarfed when looking at energy derivatives trading. If EEX is even analyzed, it is clear that the same players of other exchanges are in place. The EEX main shareholder is Deutsche Börse Group with 75% of the shares, followed by Edison S.p.A., Enel Global Trading S.p.A. (Italy), and 3 Austrian organizations. Deutsche Börse Group’s shareholders are 90% institutional shareholders, of which 36% are from North America and 25% are from Great Britain. If you now analyze EEX, it becomes clear that it is directly linked to major Russian traders. Of the 424 participants, the main heavyweights include Gazprom Austria GmbH, Gazprom Marketing & Trading Limited, Gazprom Marketing & Trading Switzerland AG, and Novatek Gas & Power GmbH. The EEX also holds key financial organizations with their own spot and derivatives arms, such as BofA Securities Europe SA, Citadel Energy Investments, Citigroup Global Markets, Goldman Sachs Bank Europe SE, Goldman Sachs International, J.P. Morgan, Mizuho Securities USA, Morgan Stanley, Societe Generale International, etc. When it comes to energy trading in Europe, international financial players are holding all the cards and are able to influence (or manipulate) the market.

Current price spikes are not abnormal if it is understood that all financial players have been betting on higher prices since the beginning of this year. Goldman Sachs pitched a commodities “supercycle” in April 2021, JPMorgan followed a bit later. All other major financials followed suit very soon after, leading to a legal but pushy energy price spike expectation. These forecasts were made even at times when physical markets, oil especially, did not demonstrate crude oil shortages. As several analysts repeatedly stated, US markets don’t need a lot of crude oil storage. Fluctuations in the USA were seasonable. At the same time, storage reports in Fujairah, Singapore, and Japan, indicated “normal” physical storage situations.

Just after Gazprom’s condensate processing facility in Siberia was destroyed, the crude oil hysteria jumped to natural gas. Crisis reports started to emerge in the market. These reports seem to have been very well understood by Russian parties, as Gazprom decided to put pressure on the physical gas market, expecting financial markets to move very soon after. International traders, such as Vital, Glencore, and Trafigura, were looking at that time at extreme risks in their portfolios, as there were large short positions on gas and power in the financial markets. Reports emerged last week that Gunvor, the largest independent LNG trader, is back in the debt markets, for the 1st time since 2013. Zerohedge stated that Gunvor is facing massive margin calls as the global natural gas arb explodes. Possible casualties are ABNAmro, Credit Agricole, Rabobank, SG, Natixis, ING, and Unicredit. The site reports also that the margin calls are between $3.6B and $6.1B in the coming months for a company with a $2.5B net equity.

The natural gas crunch in Europe may well be a self-made issue. To increase the influence of financial markets over energy markets is to increase the risk of volatility. With a huge uncontrolled OTC market in place, with immense volumes of financials swaps being traded, with re-hedging by swap-dealers, and nearly 70% of trading volume coming from algorithmic trading, the threat to natural gas markets is clear.

It is possible that Russia combined its potential physical gas market manipulation with its ability to influence financial markets. It is unclear which came first, but a combination of both, clearly not understood by unprepared European politicians, has given Russia a potent geopolitical weapon. By understanding the fundamentals of both sides, extreme energy price spikes are easy to realize. By understanding that algorithms now control the financial market and that the natural gas market is no longer focused on physical trades but on paper trading, Russia is able to move markets. Most algorithms of traders are linked to certain market keywords, events, or price level red lines. They act automatically, in principle to prevent spikes or huge losses on respective futures holdings. In the current European energy crunch, Russia seems to have been able to tweak the system to its own advantage. In the past, Putin’s response to a new energy market was, “if Europe wants a liberalized open energy market, let’s have it”. Now, he is all too happy to point out that “Europe’s current energy crunch is its own doing, now deal with your own strategy”. Claims by the IEA that Russia is unable to provide more natural gas have not be proven. Russia is currently using all the instruments at its disposal to prove that Russia’s energy weapon is ready and armed.

In the coming months, the weaponization threat of a fully financialized energy market needs to be assessed, and measures to prevent a repeat of current events should be taken. Handing over total control of energy prices and volume trades to paper, based on algorithms, is clearly a problem that needs to be resolved.