Over the past decade, low interest rates attracted borrowers to leveraged credit markets, which have since reached an unprecedented size and risk. The collision of a highly leveraged corporate sector with the severe economic shock from COVID-19 has created unique financial problems. This column analyses the main vulnerabilities in the loan market and evaluates the current US government response. Although the current stimulus programmes are significant, they can be improved to better target at-risk businesses, mitigate moral hazard, and optimise the level of direct government funding.

Financial frictions were at the heart of the 2008 crisis. Then, a relatively small shock triggered a devastating chain reaction that a year later brought to a halt a weak, interdependent, and obscure banking system. The shock we experience today is fundamentally more economic, directly impacting virtually all firms, consumers, and investors at their very core and with unprecedented speed. While the role of financial fragility is not the centrepiece of today’s challenges, there are important financial frictions that are affecting a significant part of the corporate sector and, if not addressed, could amplify the initial economic shock and slow down economic recovery.

The problem is that the global corporate sector has been caught in the COVID-19 shock with unprecedented levels of financial leverage. This has emerged as a result of a decade-long environment of low interest rates and elevated risk-taking. According to S&P, global debt on non-financial corporations was $71 trillion at the end of 2018, up 15% from 2008 and representing 93% of global GDP. Of this, we estimate that almost $6 trillion sits on the balance sheets of companies that would be characterised as highly leveraged.1 This segment represents the most troubling financial battleground of the pandemic crisis, as high leverage threatens to amplify distress and impede access to new capital.

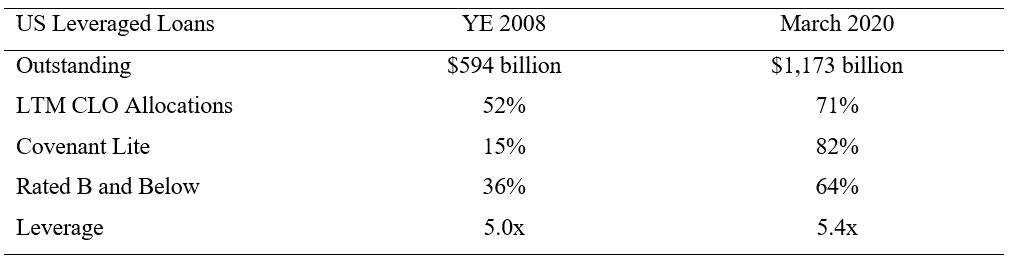

Notably, the risk profile of debt in the leveraged credit segment has increased since the last downturn, as reflected in higher leverage ratios and lower credit ratings. (See Figure 1) During prior cycles, such deterioration forced the weakest companies to restructure, mostly due to actual or impending breaches in debt covenants (Takacs 2011). But the last decade of robust debt markets came hand-in-hand with looser creditor governance (Ivashina and Vallee 2019). Among other signs of contractual weakness, the share of so-called ‘covenant-lite’ leveraged loans roughly quadrupled reaching 80%, essentially stripping the early warning system away from most credit agreements. Borrowers have also been able to artificially inflate their earnings for loan tests and debt incurrence through more liberal ‘EBITDA addbacks’. Thus, in this up-cycle, even as credit quality has deteriorated, defaults have remained below long-term averages and many weaker firms were able to avoid restructuring their debt when they underperformed.2 These so-called ‘zombie firms’, which are overleveraged and in some cases insolvent, are significantly more vulnerable to a shock like the one we face today.

Figure 1 US leverage loan market: Core statistics